Fintech Software Outsourcing: Models, Benefits & Challenges

FinTech is one of the most outsourced industries worldwide, driven by the need for rapid innovation, specialized expertise, and cost efficiency. Through fintech software outsourcing, companies can access skilled development teams, accelerate time-to-market, reduce operational overhead, and scale resources on demand while maintaining focus on core business growth and customer experience.

In this article, we’ll the fundamentals of fintech software outsourcing, including the types of development tasks and products commonly outsourced, key benefits and challenges, and the major cost factors that influence project budgets and long-term success.

What is Fintech Software Outsourcing?

Fintech software outsourcing is the practice of partnering with external engineering teams to design, develop, deploy, and maintain financial applications, platforms, and digital services, such as digital wallets, lending platforms, or payment gateways.

Unlike general software outsourcing, fintech software outsourcing requires a deeper understanding of financial workflows, transaction processing, fraud prevention, and regulatory obligations.

Teams must design systems that can handle sensitive financial data, maintain high availability, and support compliance requirements from day one. As a result, fintech projects typically demand stronger security practices, more rigorous testing, and greater domain expertise than standard business applications.

What Fintech Software Development Tasks Can Be Outsourced?

Fintech software outsourcing allows companies to access specialized expertise without expanding internal teams. Businesses can delegate key tasks such as product development, system integration, UX/UI design, and legacy system modernization to accelerate innovation and improve operational efficiency.

- Develop custom fintech software: Outsourcing partners can build tailored fintech solutions such as digital wallets, neobanks, payment gateways, lending platforms, blockchain applications, and investment management systems.

- Financial system integration: Many financial institutions rely on multiple platforms, legacy systems, and third-party services. Outsourcing teams can integrate APIs, payment networks, banking systems, KYC providers, and financial data platforms to enable seamless operations and improve scalability.

- Design UX/UI for fintech applications: Specialized design teams can create intuitive web and mobile interfaces that simplify complex financial processes while improving customer engagement and retention.

- Application modernization and migration: Outsourcing providers can modernize outdated applications, migrate infrastructure to the cloud, enhance cybersecurity measures, and introduce advanced features that support future business growth.

Types of Fintech Products Commonly Outsourced

Fintech companies frequently outsource the development of specialized financial products that require strong domain expertise, regulatory knowledge, and advanced technical capabilities. Below are some of the most common outsourced fintech products for outsourcing:

1. Digital payments & Mobile wallets

Digital payment solutions enable consumers and businesses to send, receive, and manage payments through web and mobile platforms. These products support online purchases, contactless transactions, peer-to-peer transfers, and merchant payment processing.

Key Features:

- One-tap checkout and QR/contactless payments

- Peer-to-peer (P2P) money transfers

- Refund, dispute, and chargeback management

- Fraud detection and settlement reporting

2. Digital banking apps (Retail & SME)

Digital banking applications provide users with a complete banking experience through mobile or web interfaces. They allow individuals and businesses to manage accounts, payments, cards, and banking services without visiting physical branches.

Key Features:

- Digital onboarding with identity verification

- Account management, transfers, and bill payments

- Card controls, transaction alerts, and secure messaging

- Administrative dashboards and audit trails

3. Lending platforms (Digital Lending, BNPL, P2P)

Lending platforms streamline the entire loan lifecycle, from application and underwriting to repayment and collections. These solutions are widely used by banks, fintech lenders, and Buy Now Pay Later (BNPL) providers.

Key Features:

- Loan applications and eligibility verification

- Automated underwriting and credit scoring

- Repayment scheduling and collections management

- Portfolio performance and risk monitoring

4. WealthTech platforms

WealthTech solutions help users invest, trade, and manage portfolios through digital channels. Many platforms incorporate automation and data-driven recommendations to improve investment decision-making.

Key Features:

- Investor onboarding and risk profiling

- Portfolio tracking and order management

- Automated rebalancing and performance reporting

- Market data and brokerage integrations

5. InsurTech solutions

InsurTech software digitizes insurance operations, making policy purchases, claims processing, and customer communication more efficient. These platforms improve customer experience while reducing operational costs for insurers.

Key Features:

- Digital quote-to-policy workflows

- Claims submission and document management

- Fraud detection and automated claim processing

- Omnichannel customer communication

6. Personal finance management (PFM) apps

PFM applications help users monitor spending habits, create budgets, track savings goals, and improve financial wellness. They provide actionable insights through consolidated financial data.

Key Features:

- Multi-account aggregation and transaction categorization

- Budgeting and savings goal management

- Spending analytics and financial health reports

- Smart notifications and automated reminders

Personal finance management apps

7. RegTech & Compliance automation platforms

RegTech solutions help financial institutions automate regulatory processes and reduce compliance risks. They improve operational efficiency while supporting audit readiness and regulatory reporting requirements.

Key Features:

- KYC/KYB verification workflows

- AML monitoring and suspicious activity alerts

- Audit logs and compliance reporting

- Governance and policy management dashboards

8. Open banking, embedded finance & BaaS platforms

These API-driven platforms allow businesses to embed financial services into existing products and applications. They enable organizations to offer payments, banking, lending, and financial data services without building core infrastructure from scratch.

Key Features:

- Consent management and secure authentication

- API orchestration and data normalization

- Partner onboarding and program management

- Monitoring, reliability, and transaction controls

Fintech Software Outsourcing Models

Choosing the right fintech software outsourcing model depends on project scope, budget control, regulatory complexity, and how much flexibility the business needs during development. Each model offers a different balance between cost predictability, delivery speed, team control, and long-term scalability.

1. Fixed-price model

The fixed-price model works best when a fintech project has a clearly defined scope, timeline, and set of features. The outsourcing partner estimates the full development cost upfront, which helps businesses control budgets before work begins.

However, because fintech products often involve compliance, integrations, and security risks, fixed pricing may include extra buffers to cover unexpected changes.

2. Time and materials model

The time and materials model is suitable for fintech projects where requirements may evolve during development. Instead of paying a fixed amount, companies pay for the actual hours spent by developers, designers, QA engineers, and other specialists.

This gives businesses more flexibility to adjust features, integrations, or compliance requirements as the product develops.

3. Dedicated team model

The dedicated team model gives fintech companies access to a stable group of external specialists who work as an extension of their internal team.

This model is ideal for long-term product development, continuous support, and complex fintech platforms that require ongoing updates, security improvements, and compliance maintenance. Costs are usually billed monthly based on the team composition.

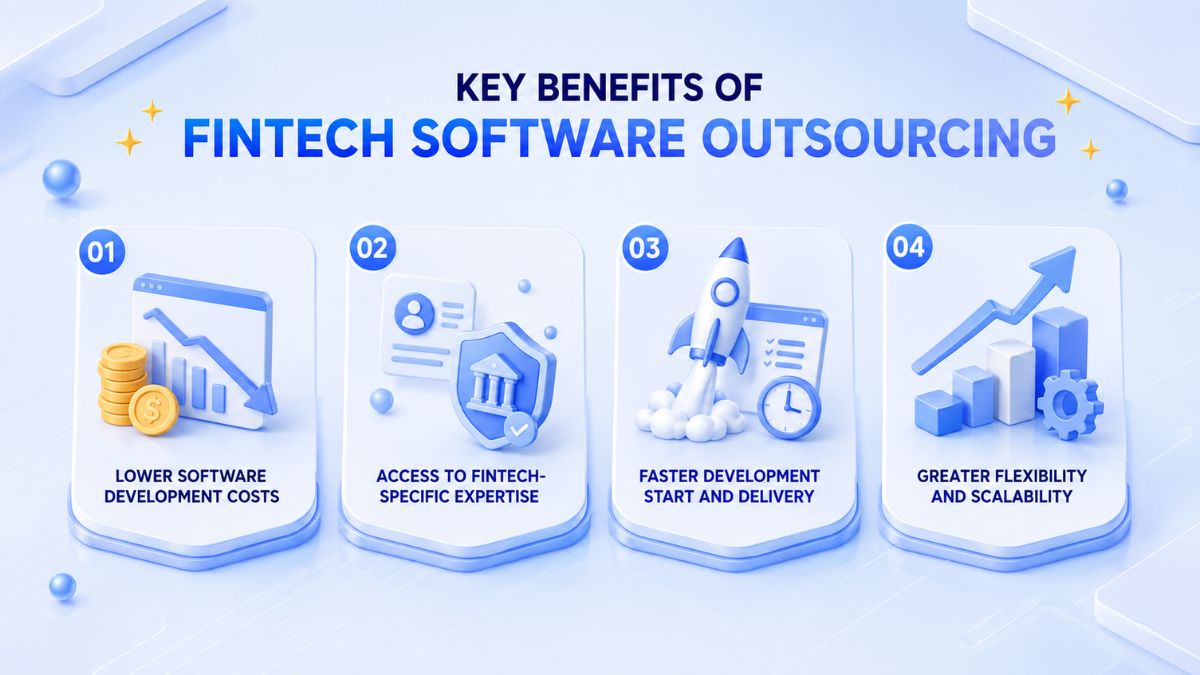

Benefits and Challenges of Fintech Software Outsourcing

Benefits of fintech development outsourcing

Fintech software outsourcing offers more than simple cost savings. For banks, startups, lenders, payment companies, and digital finance platforms, it provides access to specialized talent, faster delivery, and stronger technical execution without the burden of building every capability in-house.

Lower software development costs

Outsourcing helps fintech companies reduce expenses related to recruitment, onboarding, training, office space, payroll, and infrastructure. Instead of maintaining a full internal team, businesses pay for the development expertise they need, making it easier to control budgets and scale resources based on project demand.

Access to fintech-specific expertise

Fintech products require knowledge of financial workflows, security standards, payment systems, compliance requirements, and user trust. Outsourcing partners with fintech experience can bring developers, QA engineers, designers, business analysts, and project managers who understand how to build secure and scalable financial software.

Faster development start and delivery

Outsourcing allows fintech companies to begin development without spending months hiring and training internal teams. With established processes, ready-to-work specialists, and Agile delivery methods, external teams can help launch MVPs, integrations, or full-scale platforms faster than many newly built in-house teams.

Greater flexibility and scalability

Fintech projects often change as market needs, regulations, and customer expectations evolve. Outsourcing makes it easier to scale the team up or down, add specialized roles, or adjust the product roadmap without long-term hiring commitments.

Challenges when outsourcing fintech software

While fintech software outsourcing can reduce costs and speed up delivery, it also introduces risks that must be managed carefully. Because fintech products handle sensitive financial data, complex integrations, and strict compliance requirements, companies need strong governance from the beginning.

Loss of technical control and dependency on vendors

When external teams build fintech modules without full visibility into the broader platform, they may make technical decisions that work locally but create long-term technical debt. If the vendor becomes the only team that understands key integrations, switching providers or moving development in-house can become extremely difficult.

How to overcome it: Keep architecture ownership internally, require clear technical documentation, and establish continuous knowledge transfer from the first development sprint.

Increased security risks from third-party development

Financial services remain a prime target for cybercriminals, accounting for nearly 19% of all cyberattacks in 2024 (Statista). Third-party vendors can further increase the attack surface through unpatched dependencies, weak testing environments, subcontractors, or insecure development practices. In fintech outsourcing, a vendor’s security posture has a direct impact on the overall risk profile of the product.

How to overcome it: Run vendor security audits, enforce secure coding standards, review dependencies, limit access rights, and require regular penetration testing and incident response procedures.

Compliance and regulatory challenges

Outsourcing development does not transfer compliance responsibility away from the fintech company. If a vendor misunderstands requirements such as data residency, KYC, AML, privacy, or audit obligations, the fintech business remains legally accountable for the consequences.

How to overcome it: Define compliance requirements in the contract, involve legal and compliance teams early, verify the vendor’s fintech regulatory experience, and conduct regular compliance reviews throughout development.

Security and Compliance Considerations in Fintech Software Outsourcing

Unlike other industries, fintech companies must protect sensitive financial data while complying with complex regulatory frameworks across multiple jurisdictions. Since outsourcing does not transfer accountability, fintech organizations remain fully responsible for data protection, regulatory compliance, and operational resilience even when development is handled by external teams.

Establish regulatory requirements before development begins

Compliance should be incorporated into project planning, architecture design, and development workflows from the outset. Outsourced teams must understand the regulatory landscape governing the product, including payment regulations, privacy laws, and industry-specific requirements before a single line of code is written.

Common frameworks include:

- PCI DSS for payment card data protection

- GDPR and regional privacy regulations

- SOC 2 Type II security controls

- ISO/IEC 27001 information security standards

- Local financial regulations from authorities such as FCA, OCC, MAS, RBI, or APRA

Define data ownership and data residency policies clearly

Financial institutions must maintain complete control over where customer data is stored, processed, and accessed. Data residency requirements vary by country, making it essential to establish governance policies that align with local regulations and internal security standards.

Key controls include:

- Clearly documented data residency rules

- Segregated production, staging, and development environments

- Role-based access control (RBAC)

- Least-privilege access management

Implement a shared security architecture

While development activities may be outsourced, security accountability remains with the fintech organization. External teams should operate within predefined security frameworks rather than creating independent security standards that may conflict with internal policies.

Security best practices include:

- Secure API gateways and service-to-service authentication

- Encryption for data at rest and in transit

- Centralized logging and monitoring

- Secure secrets management and credential storage

- Regular penetration testing and vulnerability assessments

Maintain continuous audit readiness

Regulatory audits are not one-time events in the financial sector. Fintech products must maintain ongoing compliance through detailed documentation, transparent development processes, and traceable change management practices.

Essential audit requirements include:

- Up-to-date technical and compliance documentation

- Version control and change management records

- Traceability between requirements, code changes, and approvals

- Automated audit logs and compliance reporting

Strengthen third-party risk management

Regulators increasingly evaluate third-party vendors as extensions of a fintech company’s operational risk environment. As a result, outsourcing providers should undergo the same level of scrutiny as internal teams handling sensitive systems or customer data.

Risk management measures include:

- Vendor security assessments and due diligence reviews

- Periodic compliance audits

- Security questionnaires and control evaluations

- Contractual clauses covering breach notification and remediation responsibilities

Address AI and automated decision-making risks

As fintech companies increasingly adopt AI for lending, fraud detection, customer support, and risk analysis, additional governance controls become necessary. Regulators are placing greater emphasis on transparency, fairness, and accountability in automated financial decisions.

Key AI governance considerations include:

- Clear ownership of models and training data

- Explainability of AI-driven decisions

- Monitoring for model drift and bias

- Auditability of automated decision processes

How to Choose the Right Fintech Software Outsourcing Partner

Choosing the right partner for fintech software outsourcing requires more than comparing hourly rates or development portfolios. Fintech products involve sensitive data, payment flows, regulatory controls, audit requirements, and long-term operational risks, so the vendor must be evaluated as a strategic technology and compliance partner.

1. Look for industry-specific financial technology expertise

A strong outsourcing partner should have direct experience building products in regulated financial environments. Look for teams that can explain how they handled payment logic, customer data protection, audit trails, identity verification, compliance workflows, and financial integrations in previous projects.

Key indicators include:

- Fintech case studies across banking, payments, lending, insurance, or WealthTech

- Experience managing regulated data and financial transaction workflows

- Demonstrated examples of security, compliance, or audit-driven implementation decisions

2. Verify their approach to risk, security, and regulatory standards

In fintech, security and compliance must be embedded into daily development rather than treated as final-stage reviews. The right partner should demonstrate how they manage data access, environment separation, secure coding practices, vulnerability testing, and regulatory requirements throughout the software lifecycle.

Areas to evaluate:

- Knowledge of PCI DSS, GDPR, SOC 2, ISO/IEC 27001, and other relevant regulations

- Established secure SDLC practices, code reviews, and penetration testing procedures

- Robust controls for encryption, access management, monitoring, and incident response

3. Ensure clear accountability and project oversight

Fintech outsourcing projects often encounter challenges when responsibilities are not clearly defined. Before engagement begins, establish ownership for architecture, security decisions, compliance approvals, scope management, and risk escalation.

Important considerations:

- Clearly defined responsibilities across client and vendor teams

- Formal escalation paths for delivery risks, delays, and compliance issues

- Change management processes that support business objectives and regulatory requirements

4. Evaluate their ability to work within your organization

The most effective fintech outsourcing partners operate as an extension of internal product, engineering, compliance, and operations teams. They should integrate seamlessly with existing workflows instead of functioning as a separate delivery organization.

Signs of strong collaboration include:

- Compatibility with existing project management and engineering platforms

- Consistent communication with product, security, and compliance stakeholders

- Transparent reporting on progress, risks, blockers, and delivery milestones

5. Assess expertise in advanced analytics and intelligent systems

If the fintech product relies on AI for credit scoring, fraud detection, personalization, robo-advisory services, or customer support, the outsourcing partner must understand both technical and regulatory implications. This includes explainability, governance, bias management, and audit readiness.

Areas of focus:

- Defined ownership of models, training datasets, and generated outputs

- Explainable decision-making processes suitable for regulated environments

- Monitoring frameworks for model drift, performance changes, and ongoing updates

6. Consider long-term maintenance and operational reliability

Fintech software requires continuous maintenance because regulations, integrations, customer expectations, and security threats evolve over time. A reliable outsourcing partner should provide structured support beyond the initial launch.

Evaluate their ability to provide:

- Ongoing maintenance, monitoring, and operational support

- Knowledge transfer processes for internal teams

- Adaptation to regulatory changes, market shifts, and product evolution

7. Choose a partnership model that supports sustainable growth

Cost overruns often result from unclear scope definitions, weak change management, or pricing structures that do not match project needs. The right outsourcing partner should provide transparency around costs, scope adjustments, and long-term engagement terms.

Review the following elements:

- Pricing structures such as fixed-price, time-and-materials, or dedicated-team models

- Processes for managing and approving scope changes

- Contract terms covering IP ownership, documentation, transition support, and exit planning

Fintech Software Outsourcing Cost Factors

The cost of fintech software outsourcing varies significantly depending on product complexity, regulatory requirements, security expectations, and integration needs. While pricing differs across vendors and regions, fintech projects generally fall into several broad investment ranges that can help organizations estimate budgets before entering vendor discussions.

| Fintech Software Type | Estimated Cost (USD) | Key Features |

| Fintech MVP Development | $60,000 – $150,000 | User authentication, basic payment workflows, account management, MVP dashboards, limited third-party integrations |

| Core Fintech Platform Development | $150,000 – $400,000+ | Customer-facing applications, payment processing, transaction management, API integrations, compliance controls, analytics dashboards |

| Enterprise Fintech Software | $400,000 – $1M+ annually | Multi-region deployment, advanced security architecture, regulatory compliance management, enterprise integrations, scalability and operational support |

| AI-Powered Fintech Solutions | $100,000 – $300,000+ | Fraud detection, credit scoring, predictive analytics, personalization engines, model governance, explainability and audit capabilities |

What drives fintech software outsourcing costs?

Several factors influence fintech development costs more significantly than hourly development rates. Understanding these variables helps businesses estimate budgets more accurately and avoid unexpected expenses during implementation.

- Regulatory and compliance requirements: Standards such as PCI DSS, GDPR, AML, and KYC require additional security controls, testing, and documentation. More compliance obligations generally mean higher costs.

- Integration complexity: Connecting with banks, payment gateways, credit bureaus, and legacy systems requires extra development and testing effort. Complex integrations often extend project timelines.

- Security expectations: Fintech applications need strong encryption, access controls, audit logs, and security testing. These safeguards are essential but increase development expenses.

- Outsourcing engagement model: Fixed-price projects offer predictable budgets, while dedicated teams and time-and-materials models provide flexibility. The chosen model affects overall cost management.

- AI and advanced data processing requirements: AI features such as fraud detection or predictive analytics require data engineering, model development, and ongoing maintenance. These capabilities add to project costs.

- Post-launch support and compliance maintenance: Ongoing updates, monitoring, security patches, and compliance adjustments require continuous investment. Maintenance should be included in long-term budgeting.

Why Partner with Newwave Solutions for Fintech Software Outsourcing

Fintech companies need a partner with strong engineering capabilities, deep domain understanding, security discipline, and a commitment to consistent delivery. This is where Newwave Solutions becomes a powerful choice.

We bring more than a decade of experience delivering digital solutions across banking, payments, lending, investment, and insurance. Our teams build secure, compliant, and scalable financial platforms with cloud-native architectures, advanced analytics, and AI-enabled features.

Our expertise covers the entire lifecycle from idea to launch and continuous improvement. Whether you require fintech software development services, modernization of legacy systems, advanced integration, or full product engineering, we deliver predictable outcomes through an agile and transparent model.

Clients choose Newwave Solutions because:

- We turn fintech complexity into practical product execution: From fraud prevention and risk modeling to regulatory workflows and secure payment integrations, we help clients build fintech solutions that are not only functional but also reliable, scalable, and ready for real-world financial operations.

- We give clients access to experienced global fintech teams: Our senior engineers, strong English-speaking teams, and proven fintech expertise help clients move faster without the cost and delay of building large in-house teams.

- We build with security and governance from day one: Backed by ISO 27001 and structured delivery processes, we embed security, access control, documentation, and governance into the development lifecycle.

- We help clients launch faster without sacrificing quality: Our delivery approach focuses on clear planning, efficient execution, and rigorous QA, enabling clients to release products on time while maintaining performance, usability, and stability.

- We support full-cycle fintech innovation: We support clients across the full product lifecycle, allowing businesses to move from idea to launch and continuous improvement with one trusted technology partner.

Get in touch with our experts today to discuss your goals and discover the most efficient path from concept to market-ready fintech software solution.

Conclusion

Successful fintech products require more than strong technology. They depend on the ability to manage compliance requirements, integrate complex financial systems, maintain security standards, and adapt to changing market demands. This is why fintech software outsourcing has become a strategic approach for businesses seeking sustainable growth and faster innovation.

Achieving those outcomes starts with selecting a partner that understands both technology and the financial ecosystem. Newwave Solutions combines fintech expertise, secure development practices, and end-to-end delivery capabilities to help organizations bring ideas to market with confidence. Reach out to our experts to explore the best approach for your fintech initiative.

FAQs

What is an example of a fintech software?

An example of fintech software is a mobile banking app that lets users check balances, transfer money, pay bills, and manage cards digitally. Other examples include digital wallets, lending platforms, investment apps, and payment gateways.

How do you reduce risks in fintech outsourcing?

To minimize the risks of fintech software outsourcing, it is highly relevant to find a reliable fintech software development company with great experience in this field. All that can be successful only under proper project management conditions and clear communications for the certainty of smooth collaboration.

The risks will be further mitigated when backed by strict security measures involving confidentiality agreements and data protection compliance. Additionally, regular progress and quality tracking will ensure quality delivery by the outsourcing partner.

What is the difference between SaaS and fintech?

SaaS Development and FinTech are both part of the digital transformation, though they are oriented towards different directions: SaaS stands for software delivered over the cloud; as such, it provides subscription-based services in business needs, like customer management or project collaboration.

Fintech, in turn, describes only technology that enables and automates services related to banking, investment, or payments. The use of SaaS can be done in applications that pertain to fintech, but they do not mean the same.

What is the most commonly used fintech service?

The most used fintech services include mobile payments, digital wallets, peer-to-peer lending, and online banking. All these services are restructuring how people manage their finances, invest, and make payments. Mobile wallets and digital wallets, such as Apple Pay and PayPal, respectively, are among the most widely used fintech applications due to the convenience and security of such transactions.

What is the best framework for fintech apps?

The right selection of the framework is of prime importance for developing a scalable and secure fintech application. React Native is in demand for cross-platform mobile development, while Angular works perfectly for web applications.

Node.js and Django are widely used to build backend services owing to their speed and scalability. The best framework for the fintech app shall depend on what features are intended to be performed with the fintech app, what user experience is desired, and what security shall be addressed.

To Quang Duy is the CEO of Newwave Solutions, a leading Vietnamese software company. He is recognized as a standout technology consultant. Connect with him on LinkedIn and Twitter.

Read More Guides

Get stories in your inbox twice a month.

Let’s Connect

Let us know what you need, and out professionals will collaborate with you to find a solution that enables growth.

Leave a Reply