A Complete Guide to eWallet App Development in 2026

eWallet app development has become a strategic investment as consumers increasingly prefer fast, secure, and cashless payments. Forbes found that 53% of Americans have embraced digital wallets as their preferred payment method, surpassing traditional cards. For businesses, eWallet apps go beyond payments to enhance customer experience, boost retention, and create new revenue opportunities.

However, building a successful eWallet app requires much more than adding payment functionality. This guide covers everything you need to know before developing the app, including which wallet type to choose, what features matter, how much development costs, and which security compliance requirements must be met to launch successfully.

What is an e-Wallet App?

An e-Wallet app is a digital payment application that allows users to store, manage, and transfer money securely through a smartphone or connected device. It replaces the need for a physical wallet by keeping payment cards, bank account details, digital cash balances, and transaction records in one secure platform.

With an e-Wallet app, users can make online payments, contactless in-store purchases, peer-to-peer transfers, bill payments, and, in blockchain-enabled models, manage digital assets with faster, more transparent transactions.

Why Should You Develop an eWallet App?

Developing an eWallet app helps businesses meet rising demand for fast, secure, and flexible digital payments. As customers shift toward mobile and cashless transactions, it enhances convenience and reduces friction. It also opens new opportunities for engaging customers across both online and offline channels.

Match the shift toward cashless payments

Consumers are moving away from cash and choosing faster digital payment options. Worldpay reported that cash usage for in store purchases fell from 44% to just 15% between 2014 to 2024. An eWallet app helps businesses stay relevant in a payment landscape where mobile first transactions are becoming the norm.

Improve payment speed and user convenience

Modern customers expect payments to be instant, simple, and available inside the platforms they already use. eWallet apps support real time transactions, peer to peer transfers, and smooth in app checkouts. This can reduce friction, increase completed transactions, and improve customer satisfaction.

Build trust through stronger security

As fraud, data breaches, and regulatory scrutiny increase, users are more selective about the financial apps they trust. eWallet apps with biometrics, tokenization, encryption, and compliance first architecture can give businesses a stronger security position. This helps protect users while strengthening brand credibility.

Unlock new revenue and ecosystem growth

eWallet apps are no longer just payment tools. They can support ecommerce, embedded finance, loyalty programs, subscriptions, merchant partnerships, and digital asset services. For businesses, eWallet app development can become a strategic way to expand revenue channels and build a connected financial ecosystem.

>>>Read more: Digital Wallet App Powered by Blockchain for Smart Staking

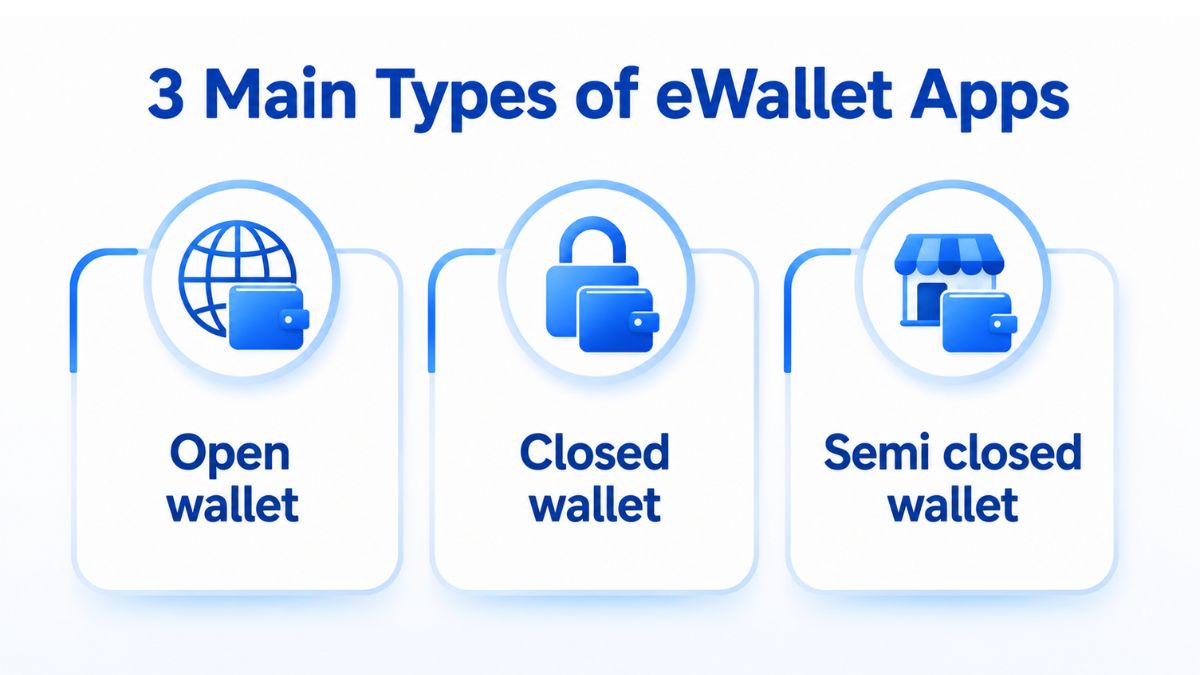

3 Main Types of eWallet Apps

eWallet apps can be built in different models depending on who issues the wallet, where users can spend the balance, and how transactions are controlled. Below are 3 main types of eWallet, including open wallets, closed wallets, and semi closed wallets.

Open wallet

Open eWallets, such as Apple Pay and Paypal, offer the highest level of flexibility and are typically issued by banks or licensed financial institutions. Users can store funds, make payments, transfer money to other wallets or bank accounts, and even withdraw cash from ATMs.

Closed wallet

Closed eWallets are developed by a specific business and can only be used within that company’s ecosystem. They are commonly used for purchases, refunds, loyalty rewards, or stored credits, helping businesses improve customer retention and encourage repeat transactions. Notable examples are Amazon Pay and Starbucks Rewards.

Semi closed wallet

Semi-closed eWallets, such as Google Pay, Paytm, and PhonePe, allow users to make payments within a network of authorized merchants and service providers. While they support both online and offline transactions, they generally do not allow cash withdrawals or unrestricted bank transfers.

Key Features of eWallet Apps

eWallet applications are built around three core goals: secure digital payments, seamless money movement, and enhanced financial engagement. Modern wallets combine payments, identity, and financial tools into a single ecosystem.

Instant peer-to-peer (P2P) transfers

eWallet apps enable users to send and receive money instantly using phone numbers, QR codes, or user IDs. This removes dependency on traditional banking delays and improves transaction speed.

Merchant payments (QR / NFC / In-App Checkout)

This is a mechanism that enables users to complete purchases digitally at both physical and online merchants. It typically supports QR scanning, NFC tap, or embedded checkout APIs. Beyond convenience, it standardizes cashless transactions across fragmented retail environments and directly connects wallet ecosystems to real-world commerce volume.

Bank account & Card linking

This feature connects the wallet to external financial systems such as debit cards, credit cards, and bank accounts. Without this integration, wallets remain closed systems, so interoperability is essential for mainstream adoption.

Multi-currency & Cross-border ayments

Advanced eWallets support multi-currency balances and international transfers, allow allows users to hold, convert, and transact in different currencies within the same wallet environment. This feature is critical for global users, freelancers, and remittance markets, enabling faster and cheaper cross-border transactions compared to traditional banking channels.

Multi-factor authentication & Biometric Security

Modern wallets use PIN, OTP, fingerprint, and facial recognition to secure access and authorize transactions. This reduces fraud risk and ensures only verified users can execute payments.

End-to-end encryption & Tokenization

Sensitive financial data is encrypted using advanced protocols, while tokenization replaces card details with secure digital tokens during transactions. This feature protects users from data breaches and payment interception risks.

Transaction history & real-time tracking

Every movement of money inside the wallet is automatically recorded and displayed in a structured history feed. Users can see where the money went, when it was sent, and what type of transaction it was. Some systems also update this in real time, so balances adjust instantly after each payment.

Budgeting & Spending insights

Beyond just showing history, some wallets organize transactions into categories like food, transport, shopping, or bills. Over time, the app can show patterns such as where most money is spent or how spending changes monthly. Users may also set limits to control specific categories.

Rewards, cashback & Loyalty programs

Many eWallets include incentive systems where users earn cashback, discounts, or points for making payments. These rewards are usually tied to specific merchants or spending categories and are automatically applied after transactions.

Merchant APIs & Integration layer

eWallets often provide APIs or SDKs that allow merchants and platforms to integrate payment functionality directly into their systems. This means a ride-hailing app, an online store, or even a SaaS product can accept wallet payments without building payment infrastructure from scratch.

Multi-device synchronization

Users today expect their financial data to follow them across devices. Whether they log in from a phone, tablet, or web dashboard, their balance, transaction history, and settings remain synchronized. Any action taken on one device is instantly reflected on others.

How Much Does It Cost to Develop an eWallet App

The cost to develop an eWallet app usually ranges from $40,000 to $300,000, depending on app complexity, payment features, security requirements, third party integrations, and platform coverage. Here’s a cost breakdown based on the app complexity level.

|

Level of Complexity |

Estimated Cost |

Timeline |

Key Features |

|

Basic |

$40,000 to $60,000 |

2 to 4 months |

Clean interface, simple navigation, core features only, standard security, basic data storage, push alerts, supports either iOS or Android |

|

Moderate |

$60,000 to $120,000 |

4 to 6 months |

Improved interface, smoother navigation, added core features, stronger security, API integrations, supports both iOS and Android |

|

Complex

|

$120,000 to $300,000

|

6 to 9 months

|

Premium UI UX design, tailored payment features, advanced security architecture, third party service integrations, real time transaction updates, reporting and analytics, and compatibility across multiple devices. |

Key factors affecting eWallet app development cost

Several factors influence the final cost of eWallet app development, from design complexity and backend architecture to security, compliance, and platform choice. Understanding these cost drivers helps businesses plan a realistic budget and prioritize the features that matter most for launch.

- Design complexity: A simple interface costs less to build, while a custom UI UX with advanced user flows, animations, and branded visuals requires more design time.

- Backend development: A scalable backend that supports high transaction volume, real time updates, and analytics will increase development cost but is essential for long term stability.

- Third-party integrations: eWallet apps often need payment gateways, banking APIs, KYC providers, push notification tools, GPS services, or analytics platforms. Each integration adds cost because it requires secure implementation, compatibility testing, and ongoing maintenance.

- Security measures: Features such as encryption, biometric login, multi factor authentication, tokenization, fraud detection, and secure data storage require deeper technical expertise and more testing.

- Compliance requirements: eWallet apps must follow payment, privacy, and financial regulations depending on the target market. Compliance work may include GDPR, PSD2, KYC, AML, audit logs, user consent management, and secure API standards.

- Platform selection: Development cost depends on whether the app is built for iOS, Android, or both. Native development can offer stronger performance, while cross platform frameworks may reduce cost and speed up delivery for MVPs.

- Technology stack: Basic stacks are usually more affordable, while advanced technologies such as AI, blockchain, machine learning, or real time analytics increase cost but enable more sophisticated features.

- Feature complexity: Core features such as wallet top up, payment history, and notifications cost less than advanced functions. P2P transfers, multi currency wallets, budgeting tools, loyalty programs, crypto support, and merchant dashboards require more design, development, and testing effort.

Step-by-step Guide for eWallet App Development

Building an eWallet app involves market validation, secure architecture, regulatory planning, careful development, and continuous support after launch. Below is a practical process businesses can follow to build a reliable and scalable eWallet solution.

Step 1: The discovery phase

The discovery phase defines the product direction before development begins. At this stage, businesses research the market, analyze competitors, study target users, review legal requirements, and identify the wallet features that best match user needs.

Key activities include:

- Conduct market, competitor, and user research to find demand, pain points, and product gaps.

- Define core features such as account management, transaction history, wallet top up, P2P transfer, and notifications.

- Review compliance needs, choose the target platform, and estimate budget, timeline, and development scope.

Step 2: Architecture and design

This step turns business requirements into a clear product structure and user experience. The team defines app architecture, user flows, wireframes, prototypes, and the design system to ensure the eWallet is easy to navigate and secure to use.

This step includes:

- Create user journeys for registration, KYC, wallet top up, payment, transfer, and transaction tracking.

- Design wireframes and prototypes with a focus on clarity, trust, and low friction payment actions.

- Plan system architecture, database structure, API flows, security layers, and integration points.

Step 3: Start eWallet app development

Development is the core phase where the eWallet app is built across frontend, backend, and payment infrastructure. The team selects the right tech stack, develops user facing screens, builds backend logic, and integrates payment gateways or banking APIs.

- Choose technology stack: Select suitable programming languages, frameworks, and platforms that support scalability, security, and future updates while aligning with the app’s functional requirements.

- Build the team: Build a skilled development team including roles such as project manager, UI/UX designer, frontend and backend developers, QA specialists, and security experts, either through in-house hiring or outsourcing.

- Develop frontend and backend: Develop frontend and backend systems by implementing user interfaces, integrating designs, building APIs, managing databases, and ensuring smooth communication between all components for reliable performance.

- Payment integration: Integrate payment gateways and financial APIs to enable secure transactions, while ensuring proper configuration, testing, and seamless user experience during payments and transfers.

- Security implementation: Implement strong security measures such as encryption, multi-factor authentication, and regular audits to protect user data, prevent fraud, and maintain compliance with financial regulations.

Step 4: Testing stage

Testing usually takes place before product release. It’s aimed at ensuring that the app functions as planned and specified by the requirements, and all inconsistencies are promptly eliminated. At this point, it’s important to test your e-Wallet app security. Since eWallet app development holds sensitive information about clients and banking, all security-related features must be thoroughly tested here.

Step 5: App launch

Once testing is complete, the app moves into the release phase, where deployment varies based on the platform. Launching on iOS typically involves a stricter review process with detailed compliance checks, which can take longer for approval.

In contrast, Android apps on Google Play usually have a faster and more flexible approval cycle. For cross platform or hybrid apps, developers must follow the submission guidelines for both ecosystems separately.

Step 6: Support and maintenance stage

This is the process of upgrading and improving your end product that your eWallet app development company should carry out as long as the product is used. The team helps fix issues, handle unexpected problems, and keep the app secure, stable, and compliant with evolving regulations. Continuous improvements based on user feedback and market needs also help the app stay relevant and scalable over time.

Security Compliances for Developing an eWallet Appplication

A secure eWallet app must protect users from fraud, meet regulatory requirements, and create a trusted payment environment from onboarding to every transaction. When developing a digital wallet app, it’s essential to follow the following security compliance standards:

Data protection & Security, compliance standards

An enterprise grade eWallet app should be built with strong data protection and regulatory compliance from the start. This includes encryption, tokenization, secure API gateways, access control, fraud monitoring, and regular security audits to reduce payment risks and protect user information.

Key regulations and standards include:

- PCI DSS: Required for apps that process, store, or transmit cardholder data. It helps ensure secure payment handling, encrypted card data, access control, and regular vulnerability checks.

- GDPR: Applies to businesses handling personal data of users in the European Union. It requires clear user consent, data minimization, privacy protection, and the right for users to access or delete their data.

- ISO 27001: An international standard for information security management. It helps businesses build structured processes for managing risks, protecting data, and maintaining long term security governance.

- PSD2: A key European payment regulation that supports secure electronic payments. It requires strong customer authentication and secure communication between banks, payment providers, and fintech applications.

- AML and KYC Regulations: These rules help prevent money laundering, fraud, and illegal financial activity. eWallet apps must verify user identity, monitor suspicious transactions, and keep proper compliance records.

- Local Fintech Regulations: Each target market may have its own financial licensing, data storage, reporting, and payment operation rules. Businesses must review local requirements before launching an eWallet app in a specific region.

Digital identity verification & eKYC process

A robust eKYC (electronic Know Your Customer) process is critical for open and semi closed eWallet apps because users may transfer money, store balances, or access financial services. The workflow usually includes identity document verification, biometric checks, liveness detection, and real time validation through trusted third party verification providers.

Automating eKYC helps businesses comply with AML and KYC requirements while improving onboarding speed. Instead of relying on manual checks, users can verify their identity faster, reduce drop off during registration, and access wallet services with greater confidence.

Challenges in Developing eWallet Apps & How to Solve

Developing an eWallet app requires businesses to balance speed, security, compliance, and user experience. Since the app handles sensitive financial data and real time transactions, even small technical or regulatory gaps can affect user trust, system stability, and long term growth.

Security & Data privacy

eWallet apps store and process sensitive information such as bank account details, card data, personal IDs, and transaction records. This makes them attractive targets for cyberattacks, fraud, and identity theft. A single breach can cause financial loss, legal consequences, and serious damage to brand trust.

To solve this, businesses should implement strong encryption, tokenization, multi factor authentication, biometric login, and secure data storage. Regular security audits, penetration testing, fraud monitoring, and PCI DSS compliance also help detect risks early and protect payment data.

Regulatory compliance

Fintech regulations vary by country and region, covering data privacy, payment security, consumer protection, KYC, and anti money laundering requirements. For eWallet apps, failing to meet standards such as GDPR, CCPA, PCI DSS, or local payment rules can delay launch or create legal risks.

Compliance should be planned from the discovery phase, not added at the end. Businesses should work with fintech legal experts, build automated KYC and transaction monitoring, maintain audit trails, and update compliance controls as regulations change.

Scalability & Performance

As user numbers and transaction volumes grow, an eWallet app must process payments, transfers, notifications, and account updates without delay. Poor scalability can lead to slow loading, failed transactions, system crashes, and a poor user experience during peak usage.

A flexible architecture is essential here, allowing the system to adapt as demand grows. This often involves using cloud based infrastructure, modular services, load balancing, and efficient data handling strategies. Continuous monitoring and performance testing also play a key role in identifying potential bottlenecks early and maintaining a smooth user experience as the platform scales.

Cross platform compatibility

eWallet apps need to work smoothly across different devices, operating systems, screen sizes, and network conditions. Each platform may have different security rules, performance limits, and deployment requirements, making consistent functionality harder to maintain.

A practical approach is to combine adaptive UI design with targeted platform tuning. The app should adjust to different screen sizes and device capabilities while still leveraging native features where they add value. Continuous testing across devices, operating systems, and varying network conditions helps catch inconsistencies early, and ongoing updates ensure the app remains stable, secure, and compatible over time.

Newwave Solution – a Reliable eWallet App Development Company

If you are planning to develop an eWallet app but are unsure where to start, partnering with professional experts from Newwave Solutions is a valuable solution. With over 14 years of experience in providing financial software development services, Newwave has supported numerous businesses in building and growing their own E-Wallet apps successfully.

Our team builds secure, scalable, and cross platform eWallet solutions that support seamless transactions, digital asset protection, and long-term performance. Each app is designed with flexible architecture, strong security layers, and user centered features to improve convenience, build trust, and support sustainable business growth.

To see how we develop an eWallet app in practice, here is one of our successful blockchain wallet projects delivered for a global client in the Web3 industry. The project demonstrates how we combine secure architecture, cross chain interoperability, and user focused design to build enterprise ready eWallet solutions.

- Client’s requirements: Our client needed a self custodial multi chain wallet that enables users to securely manage cryptocurrencies, tokens, and NFTs across major blockchain networks (Ethereum, BNB Chain, Polygon, TON, and Bitcoin) through mobile apps, web, and a browser extension.

- Our Solution: We designed a scalable cross platform architecture with deep multi chain integration, secure private key management, consistent user experience across devices, and optimized blockchain connectivity to deliver seamless digital asset management.

- Result: This eWallet platform effectively simplified multi chain asset management, improved accessibility across platforms, strengthened digital asset protection, and provided a reliable foundation for future Web3 and DeFi expansion.

Read the full case study: Blockchain App Wallet for Multi-Chain Success

Conclusion

The e-Wallet app is the way to manage one’s finances nowadays. It is secure, convenient, and cost-effective. If you are looking to proceed with the eWallet app development, you should consider the different aspects discussed in this article. Then, make sure to choose an experienced eWallet app development company that has the expertise and experience to develop an app that meets your requirements and budget, like Newwave Solutions.

Book a consultation with our experts to turn your eWallet app idea into a secure, scalable, and market-ready digital payment solution.

Contact Information:

- Head Office (Hanoi): 1F, 4F, 10F, Mitec Building, Cau Giay Ward, Hanoi City, Vietnam

- Branch Office (Tokyo): 1chōme118 Yushima, Bunkyo City, Tokyo 1130034, Japan

- Hotline: +84 985310203

- Website: https://newwavesolution.com

- Email: [email protected]

FAQs

How long does it take to build an eWallet app?

A basic eWallet app can usually be developed within 2 to 4 months, while a feature rich enterprise solution may require 6 to 9 months or longer. The timeline depends on the scope, compliance requirements, testing, and third party integrations.

Which type of eWallet should I build?

The right choice depends on your business model. Closed wallets work well for a single platform, semi closed wallets support selected merchant networks, and open wallets allow broader financial services such as bank transfers and cash withdrawals.

Do eWallet apps need KYC verification?

If the app handles regulated financial services, KYC verification is often required to comply with local financial laws. Automated eKYC can verify user identities faster while helping businesses meet AML and regulatory requirements.

Should I build a native or cross platform eWallet app?

Native apps generally offer the best performance and deeper platform integration for iOS and Android. Cross platform frameworks such as Flutter or React Native can reduce development time and cost while maintaining a consistent user experience.

How do eWallet apps generate revenue?

Businesses can monetize eWallet apps through transaction fees, merchant commissions, subscription plans, premium features, foreign exchange fees, and value added financial services. The best revenue model depends on the target market and business strategy.

To Quang Duy is the CEO of Newwave Solutions, a leading Vietnamese software company. He is recognized as a standout technology consultant. Connect with him on LinkedIn and Twitter.

Read More Guides

Get stories in your inbox twice a month.

Let’s Connect

Let us know what you need, and out professionals will collaborate with you to find a solution that enables growth.

Leave a Reply